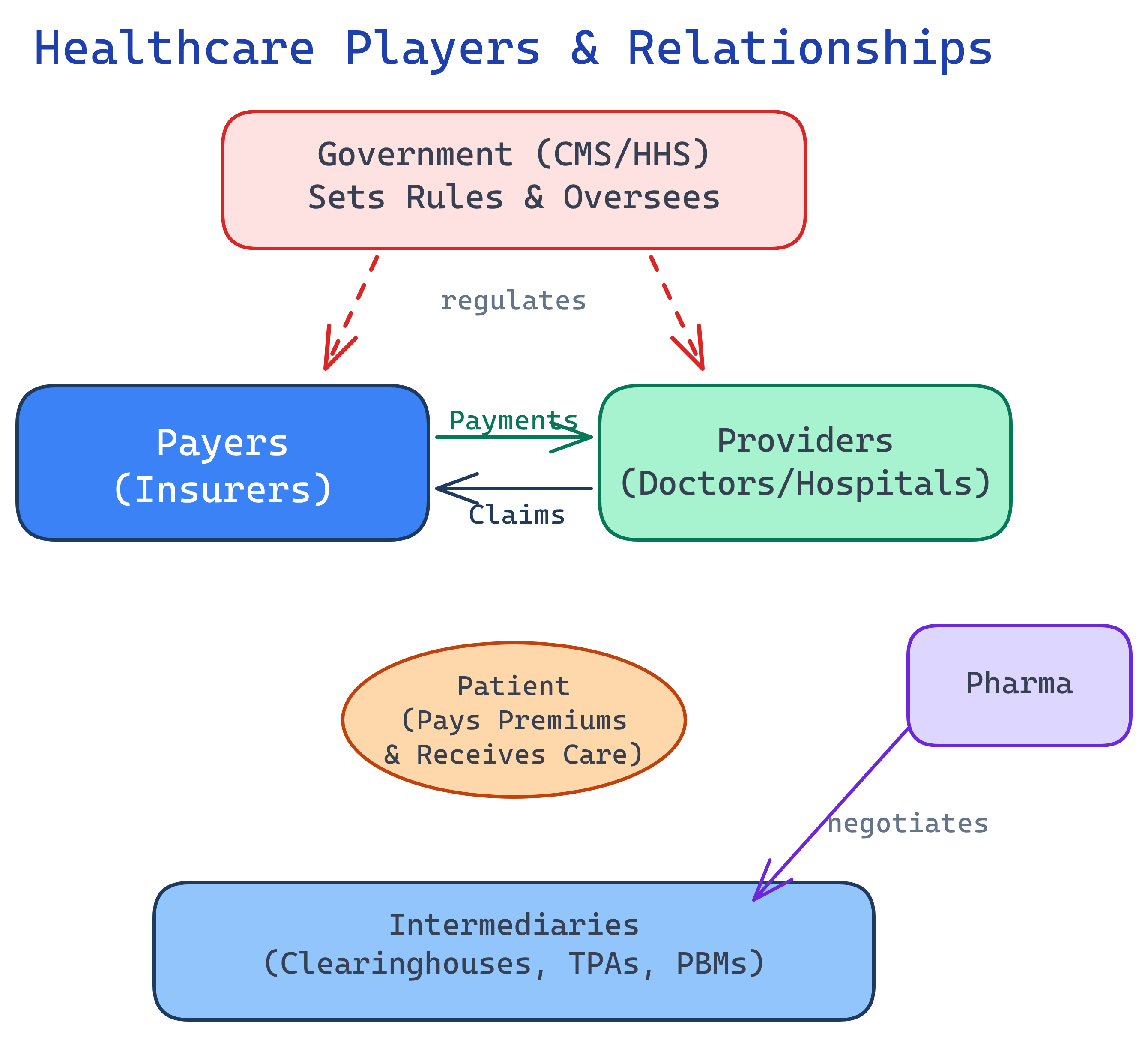

Key Players & Stakeholders

The US Healthcare system has 6 major player groups: Payers (insurance companies), Providers (doctors/hospitals), Patients, Pharma, Government (CMS/HHS/FDA), and Intermediaries (PBMs, clearinghouses, TPAs). Understanding who these players are and how they interact is the foundation for everything else in healthcare data.

Explain Like I'm 12

Picture a school play. The actors are Providers (doctors) — they perform the show. The audience is Patients — they're the reason the show exists. The ticket booth is Payers (insurance) — they collect money and pay for things. The principal is Government (makes rules everyone must follow). The costume shop is Pharma (makes medicines). And the stage crew is Intermediaries (PBMs, clearinghouses) — you never see them, but nothing works without them.

The 6 Player Groups at a Glance

Payers — Who Pays the Bills

When someone says "payer" in healthcare, they mean the entity writing the checks. Payers decide what gets covered, how much gets paid, and to whom. Here are the major categories:

Commercial Insurance (the "Big 5")

Five companies dominate commercial health insurance in the US:

| Company | Revenue (approx.) | Key Note |

|---|---|---|

| UnitedHealth Group | $372B | Largest US health insurer, also owns Optum (analytics + PBM) |

| Elevance Health (Anthem) | $170B | Blue Cross Blue Shield licensee in 14 states |

| Cigna | $195B | Owns Express Scripts (PBM) |

| Aetna (CVS Health) | $350B (CVS total) | Owned by CVS, which also owns Caremark (PBM) |

| Humana | $106B | Heavy Medicare Advantage focus |

Government Payers

- Medicare: 67 million beneficiaries (age 65+, disabled, ESRD)

- Medicaid: 90 million beneficiaries (low-income individuals and families)

- CHIP: Children's Health Insurance Program

- VA / TRICARE: Military and veterans

Self-Insured Employers

Here's a fact that surprises many people: 60% of covered workers are in self-insured plans. The employer bears the financial risk directly — they just hire a TPA (like a payer) to process claims. This matters because self-insured plans are regulated by federal ERISA law, not state insurance departments.

Managed Care Organizations (MCOs)

Most states contract with MCOs to run their Medicaid programs. The state pays the MCO a per-member-per-month (PMPM) fee, and the MCO manages care for that population. Companies like Centene and Molina dominate this space.

Providers — Who Delivers Care

Providers are the people and organizations that actually deliver healthcare services. If a payer writes the check, the provider earns it.

Hospitals

| Type | % of US Hospitals | Examples |

|---|---|---|

| Non-profit | ~49% | Mayo Clinic, Cleveland Clinic, most community hospitals |

| For-profit | ~20% | HCA Healthcare, Tenet Health |

| Government | ~18% | VA hospitals, county hospitals |

| Other | ~13% | Teaching hospitals, specialty hospitals |

Health Systems

Large integrated networks that combine hospitals, physician groups, and sometimes insurance plans. Think of Kaiser Permanente (integrated payer + provider), HCA Healthcare (largest for-profit system), and CommonSpirit Health (largest non-profit).

Individual Providers

Physicians, nurse practitioners (NPs), physician assistants (PAs), therapists, and other licensed clinicians. Every provider gets a unique NPI (National Provider Identifier) — a 10-digit number that follows them throughout their career.

Facility vs. Professional Claims

This is a critical distinction for data professionals. When you visit a hospital:

- Facility claim (UB-04 / 837I): The hospital bills for the room, equipment, nursing staff, supplies

- Professional claim (CMS-1500 / 837P): The doctor bills separately for their professional services

One patient visit = two separate claims. If you're doing claims analytics and don't understand this, your numbers will be wrong.

Government — Who Makes the Rules

The government is both a payer (Medicare/Medicaid) and a regulator. Here are the key agencies you need to know:

| Agency | Full Name | What They Do |

|---|---|---|

| HHS | Dept. of Health & Human Services | Parent agency — oversees CMS, FDA, CDC, NIH, OIG |

| CMS | Centers for Medicare & Medicaid Services | Runs Medicare/Medicaid, sets payment rates, quality programs (HEDIS, STAR) |

| FDA | Food & Drug Administration | Drug and medical device approval |

| CDC | Centers for Disease Control | Disease surveillance, public health guidelines |

| OIG | Office of Inspector General | Fraud enforcement, exclusion lists |

| State DOI | Dept. of Insurance (per state) | Regulates commercial insurance within each state |

Pharma & Medical Devices

The pharmaceutical and medical device industries develop the drugs, biologics, implants, and diagnostic equipment that providers use to treat patients.

How Drug Pricing Actually Works

Drug pricing in the US is notoriously complex. Here's the simplified flow:

- Pharma company sets a list price (WAC — Wholesale Acquisition Cost)

- PBM negotiates a rebate in exchange for placing the drug on its formulary

- Pharmacy dispenses the drug to the patient

- Patient pays a copay; the plan pays the rest (minus the rebate the PBM keeps or passes through)

The 340B Program

Safety-net providers (community health centers, certain hospitals) can buy drugs at deeply discounted prices through the federal 340B program. This is a significant revenue source for these providers and a hot topic in healthcare policy.

Medical Devices

Companies like Medtronic, Johnson & Johnson, and Abbott develop implants (hip replacements, pacemakers), diagnostic equipment (MRI machines, lab analyzers), and surgical supplies. Devices are regulated by the FDA and tracked through unique device identifiers (UDIs).

Intermediaries — The Hidden Layer

These are the organizations most people have never heard of, but they're essential to how healthcare actually operates day to day. As a data professional, you will interact with data from these entities constantly.

PBMs (Pharmacy Benefit Managers)

The "Big 3" PBMs — CVS Caremark, Express Scripts (Cigna), and OptumRx (UnitedHealth) — manage drug benefits for health plans. They negotiate prices with drug manufacturers, decide which drugs go on the formulary, and process pharmacy claims.

Clearinghouses

Think of clearinghouses as the postal service for claims. They route electronic claims between providers and payers, validate formatting, check for errors, and translate between different EDI formats. Major players include Change Healthcare (now part of Optum), Availity, and Waystar.

TPAs (Third Party Administrators)

TPAs process claims for self-insured employers. The employer bears the financial risk, but the TPA handles the day-to-day claims adjudication, provider networks, and member services. It looks like insurance to the employee, but behind the scenes the employer is paying directly.

HIEs (Health Information Exchanges)

HIEs share patient clinical data between providers. When you visit a new doctor and they can see your records from your previous provider, an HIE probably made that possible. They use standards like HL7 and FHIR to exchange data.

Patients — The Center of It All

Every player in the system ultimately exists to serve patients. Here's how American patients get their coverage:

Coverage Breakdown

| Source of Coverage | % of US Population | Approx. People |

|---|---|---|

| Employer-sponsored | ~49% | ~160M |

| Medicaid / CHIP | ~20% | ~65M |

| Medicare | ~14% | ~46M |

| ACA Marketplace | ~10% | ~33M |

| Uninsured | ~8% | ~26M |

What Patients Pay

- Premium: Monthly cost to maintain coverage (often shared with employer)

- Deductible: Amount you pay out-of-pocket before insurance kicks in

- Copay: Fixed dollar amount per visit (e.g., $30 for a PCP visit)

- Coinsurance: Percentage you pay after meeting the deductible (e.g., 20%)

- Out-of-pocket maximum: The cap — once you hit this, the plan pays 100%

SDOH (Social Determinants of Health)

Here's something that changes how you think about healthcare data: a patient's zip code predicts their health outcomes better than their genetic code. Social Determinants of Health — income, education, housing stability, food access, transportation — affect outcomes more than clinical care alone. This is why healthcare analytics increasingly incorporates SDOH data.

Comparison: All 6 Player Groups

| Player Group | Who They Are | What They Do | Key Examples | Data They Generate |

|---|---|---|---|---|

| Payers | Insurance companies, government programs | Pay for healthcare services, manage risk | UnitedHealth, Anthem, Medicare, Medicaid | Claims, enrollment, authorization, payment data |

| Providers | Doctors, hospitals, health systems | Deliver healthcare services | Kaiser, HCA, Cleveland Clinic, your local PCP | EHR records, clinical notes, lab results, procedure data |

| Government | Federal & state agencies | Regulate, pay (Medicare/Medicaid), enforce | CMS, HHS, FDA, OIG, state DOI | Quality measures, payment rules, exclusion lists |

| Pharma & Devices | Drug & device manufacturers | Develop drugs, biologics, medical devices | Pfizer, J&J, Medtronic, Abbott | Clinical trial data, NDC codes, pricing, UDIs |

| Intermediaries | PBMs, clearinghouses, TPAs, HIEs | Connect, translate, and process between other players | CVS Caremark, Change Healthcare, Availity | Pharmacy claims, EDI transactions, eligibility checks |

| Patients | Individuals receiving care | Seek care, pay premiums/cost-sharing | 330M Americans | Demographics, coverage type, SDOH data, outcomes |

Test Yourself

Q: Name the 6 major player groups in the US Healthcare system.

Q: What's the difference between a self-insured employer and a fully-insured employer?

Q: Why do one patient visit at a hospital generate two separate claims?

Q: What is CMS, and why does the entire industry follow its lead?

Q: What do PBMs do, and why are they important for data professionals?

Interview Questions

Q: What is the role of a PBM in the US Healthcare system?

Q: Explain the difference between a TPA and a payer.

Q: What is CMS and why is it important?

Q: How does a clearinghouse fit into claims processing?